Housing in Zurich and Geneva is moderately overvalued; bubble risks grow in other developed world cities globally.

- UBS Wealth Management’s UBS Global Real Estate Bubble Index 2017 report analyzes residential property prices in 20 select urban areas around the world.

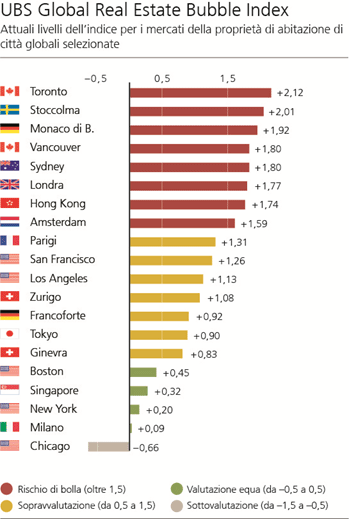

- Toronto faces the greatest risk of a housing bubble, followed in descending order by Stockholm, Munich, Vancouver, Sydney, London, Hong Kong, and Amsterdam.

- In Europe the outlook is heating up. Bubble risks are rising in Stockholm, Munich, and Amsterdam, while Paris and Frankfurt have become more overvalued since 2016. London is still at risk of a bubble but less so than last year. In contrast, Zurich and Geneva remain moderately overvalued.

Zurich, 28 September 2017 – Major urban housing markets in developed economies are still overvalued, and more are at risk of a bubble than in 2016, according to the annual UBS Global Real Estate Bubble Index from UBS Wealth Management’s Chief Investment Office.

Toronto, a new entrant, tops the Index in 2017. As in 2016, Stockholm, Munich, Vancouver, Sydney, London, and Hong Kong are also still at risk of a bubble, along with Amsterdam, which was merely overvalued last year. The only undervalued city in the study is Chicago, with three quarters of cities at risk of a bubble or overvalued.

Switzerland: No bubble risk despite one of the lowest financing costs worldwide

In Switzerland, Zurich and Geneva are moderately overvalued. Since 2012 apartment prices declined 10% in Geneva but rose 10% in Zurich. Home prices in Geneva seemed to have reached a bottom for the time being, however, and valuations increased again in recent quarters in line with re-emerging price growth. In Zurich, real prices grew at 2% over the last four quarters, slightly faster than the countrywide average.

Matthias Holzhey, Head Swiss Real Estate Investment in UBS Wealth Management’s Chief Investment Office, says: “Favorable financing conditions keep demand for home ownership buoyant. Buying a 60 square meter apartment in Zurich costs a skilled-service worker six years’ income – a low level compared to cities globally.” And, thanks to low mortgage rates, the effective financing costs are only 10% of the average annual income of a skilled service worker. But mortgage market regulations and increasing rental vacancy rates limit price upside for the time being.

Europe: Housing markets are heating up

Over the last four quarters the UBS Global Real Estate Bubble Index rose in all European cities in the study. Sharp increases were measured in Paris, Amsterdam, Frankfurt and Munich. All European cities in the study, apart from Milan, are at least in overvalued territory. London is still at risk of a bubble, albeit less so since the Brexit referendum last year.

Annual prices in Munich and Amsterdam have been growing at double digit rates, closely followed by Frankfurt (+9%). Also house prices in Stockholm have set new records and the housing market in Paris has regained nearly all ground lost since 2012.

Claudio Saputelli, Head of Global Real Estate for UBS CIO WM says: “Improving economic sentiment, partly accompanied by robust income growth in the key cities, has conspired with excessively low borrowing rates to spur vigorous demand for urban housing.” As supply is always a constraint in the most appealing cities, soaring prices has been the consequence. The combination of inexpensive financing and bullish expectations caused valuations to skyrocket and encouraged local bubble risks to grow.

Source: UBS

Optimistic expectations fuel the market

Expectations of long-term rising prices partly explain demand for housing investment in major global cities. Many market participants expect the best locations to reap most value growth in the long run buoyed by the growth of high-wealth households. Falling mortgage rates over the last decade have also made buying a home vastly more attractive. As long as supply cannot increase rapidly, many buyers see prices in the most attractive cities decoupling from rents, incomes and national price levels.

This narrative has received additional impetus in the last couple of years from a surge in international demand, especially from China, which has crowded out local buyers. An average price growth of almost 20% in the last three years has confirmed the expectations of even the most optimistic investors. “This thesis has helped fuel overvaluation and even bubble risks in most major urban housing markets in advanced economies globally”, Holzhey states. “Taking less risk in overheated markets has historically paid off on average: they delivered worse returns over a full boom-bust period than more balanced markets did”.

UBS Switzerland AG